Optimize Your Advantages with VA Home Loans: Lower Rate Of Interest Rates and Flexible Terms

Optimize Your Advantages with VA Home Loans: Lower Rate Of Interest Rates and Flexible Terms

Blog Article

The Necessary Guide to Home Loans: Unlocking the Benefits of Flexible Funding Options for Your Dream Home

Navigating the intricacies of mortgage can typically really feel complicated, yet recognizing flexible funding alternatives is important for potential house owners. With a selection of funding kinds readily available, including adjustable-rate home mortgages and government-backed alternatives, debtors can customize their funding to straighten with their individual financial conditions. These versatile choices not just give lower initial repayments however might also provide special advantages that boost ease of access to homeownership. As you take into consideration the myriad of choices, one must ask: what elements should be prioritized to guarantee the very best fit for your monetary future?

Comprehending Home Loans

Understanding home mortgage is important for possible house owners, as they represent a significant economic commitment that can affect one's monetary health and wellness for years ahead. A home mortgage, or mortgage, is a kind of financial debt that enables individuals to borrow cash to buy a home, with the building itself functioning as security. The loan provider gives the funds, and the consumer consents to repay the finance amount, plus rate of interest, over a specified duration.

Trick elements of home mortgage include the primary amount, rates of interest, car loan term, and month-to-month settlements. The principal is the initial car loan quantity, while the rate of interest establishes the cost of borrowing. Loan terms usually vary from 15 to 30 years, influencing both regular monthly settlements and overall rate of interest paid.

Kinds Of Flexible Financing

Flexible funding choices play an essential duty in fitting the diverse requirements of homebuyers, enabling them to customize their home loan remedies to fit their monetary scenarios. Among the most widespread sorts of adaptable funding is the adjustable-rate mortgage (ARM), which offers a preliminary fixed-rate period adhered to by variable rates that change based on market conditions. This can give lower first repayments, interesting those who anticipate income growth or strategy to relocate before rates readjust.

Another choice is the interest-only home mortgage, enabling debtors to pay only the rate of interest for a specific duration. This can lead to reduced regular monthly settlements originally, making homeownership more easily accessible, although it might cause bigger payments later on.

Additionally, there are likewise hybrid car loans, which incorporate features of taken care of and adjustable-rate home loans, giving security for a set term complied with by changes.

Last but not least, government-backed financings, such as FHA and VA financings, offer adaptable terms and reduced down settlement requirements, satisfying novice buyers and veterans. Each of these choices provides special advantages, permitting buyers to pick a funding remedy that straightens with their long-term personal situations and economic objectives.

Advantages of Adjustable-Rate Mortgages

How can adjustable-rate home mortgages (ARMs) profit homebuyers looking for inexpensive financing alternatives? ARMs offer the possibility for lower first interest prices compared to fixed-rate mortgages, making them an appealing option for customers aiming to lower their monthly payments in the early years of homeownership. This preliminary period of lower prices can dramatically boost price, allowing property buyers to invest the cost savings in other concerns, such as home enhancements or cost savings.

Furthermore, ARMs usually feature a cap framework that restricts just how a lot the rate of link interest can boost during adjustment periods, providing a degree of predictability and defense versus extreme fluctuations in the market. This feature can be particularly advantageous in a rising rate of interest setting.

Moreover, ARMs are optimal for purchasers who plan to refinance or sell prior to the loan readjusts, enabling them to maximize the lower prices without direct exposure to prospective rate rises. Therefore, ARMs can function as a strategic economic device for those who fit with a level of risk and are aiming to optimize their acquiring power in the present housing market. On the whole, ARMs can be an engaging option for wise property buyers seeking adaptable funding remedies.

Government-Backed Financing Choices

FHA loans, insured by the Federal Housing Administration, are perfect for first-time homebuyers and those with lower credit report. They generally require a lower deposit, making them a preferred choice for those who may have a hard time to save a considerable quantity for a standard funding.

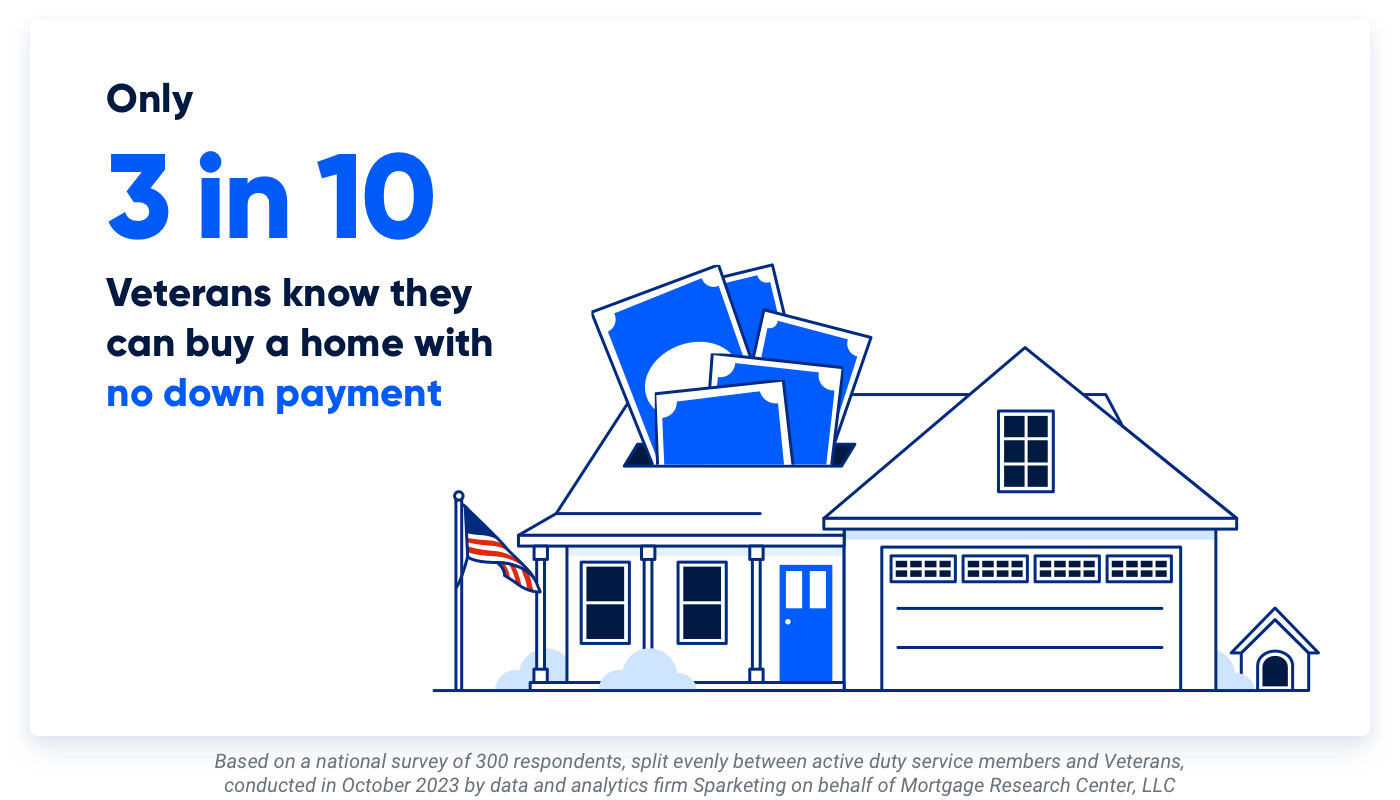

VA financings, readily available to experts and active-duty army employees, use positive terms, including no private home mortgage and no down settlement insurance coverage (PMI) This makes them an appealing choice for eligible consumers looking to acquire a home without the problem of extra costs.

Tips for Selecting the Right Lending

When examining lending choices, consumers typically gain from thoroughly evaluating their economic circumstance and long-lasting objectives. Start by identifying your spending plan, that includes not only the home purchase price yet also extra expenses such as building taxes, insurance coverage, and upkeep (VA Home Loans). This thorough understanding will certainly browse around this site guide you in selecting a finance that fits your economic landscape

Next, consider the types of financings available. Fixed-rate home loans use security in monthly payments, while variable-rate mortgages may offer lower initial rates but can fluctuate in time. Evaluate your risk tolerance and how much time you plan to remain in the home, as these variables will certainly influence your financing selection.

In addition, look at rate of interest and charges connected with each car loan. A lower rates of interest can considerably reduce the total price with time, however be mindful of closing prices and various other charges that might offset these financial savings.

Verdict

In conclusion, browsing the landscape of home lendings exposes numerous versatile financing choices that provide to diverse debtor needs. Comprehending the intricacies useful site of various lending types, consisting of government-backed car loans and adjustable-rate home mortgages, enables notified decision-making.

Browsing the intricacies of home loans can typically really feel complicated, yet comprehending versatile funding alternatives is essential for potential property owners. A home finance, or home mortgage, is a kind of debt that allows individuals to borrow money to buy a residential or commercial property, with the building itself offering as security.Trick parts of home financings consist of the principal amount, interest rate, car loan term, and regular monthly repayments.In conclusion, navigating the landscape of home lendings reveals numerous flexible financing alternatives that provide to varied customer needs. Understanding the intricacies of various loan types, consisting of government-backed loans and adjustable-rate home mortgages, makes it possible for notified decision-making.

Report this page